Covariance¶

Covariance is a measure of how much two random variables vary together. It's similar to variance, but where variance tells you how a single variable varies, covariance tells you how two variables vary together.

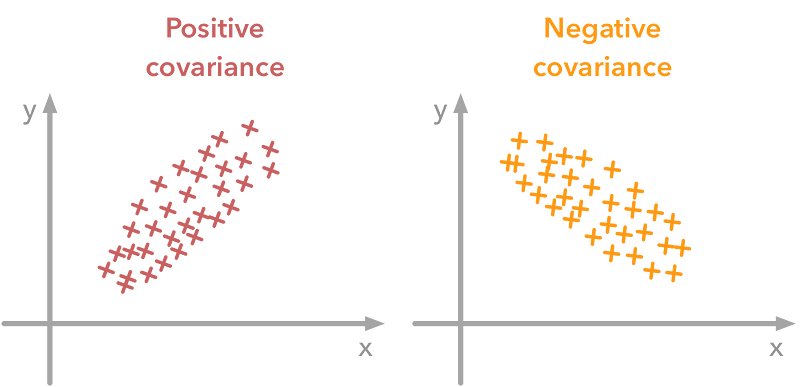

A positive covariance means that the two variables at hand are postively related, and they move in the same direction.

A negative covariance means that the two variables are inversely related, or that they move in opposite directions.

The formula to calculate covariance is as follows, $$ cov_{x, y} = \frac{ \sum (x_i - \bar{x})(y_i - \bar{y})}{N - 1} $$